-

-

The Forum works well on MOBILE devices without an app: Just go to: https://forum.tsptalk.com

-

Please read our AutoTracker policy on the IFT deadline and remaining active. Thanks!

-

$ - Premium Service Content (Info) | AutoTracker Monthly Winners | Is Gmail et al, Blocking Our emails?

Find us on: Facebook & X | Posting Copyrighted Material

-

Join the TSP Talk AutoTracker: How to Get Started | Login | Main AutoTracker Page

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Show-me Account Talk

- Thread starter Show-me

- Start date

- Status

- Not open for further replies.

Show-me

TSP Legend

- Reaction score

- 104

Zoellick Says U.S. Dollar’s Primacy Not a Certainty (Update1)

By Daniel Whitten

Sept. 27 (Bloomberg) -- World Bank President Robert Zoellick said the U.S. shouldn’t take for granted the dollar’s status as the world’s main reserve currency.

In remarks set for delivery tomorrow, Zoellick said the “next upheaval” in the international economic order is under way as emerging nations gain greater influence.

“The United States would be mistaken to take for granted the dollar’s place as the world’s predominant reserve currency,” according to excerpts released by the World Bank.

Policy makers from China to Russia repeatedly have called for an alternative to the world’s main currency in foreign- exchange reserves.

Zoellick’s speech to the Paul H. Nitze School of Advanced International Studies at Johns Hopkins University in Washington echoes his previous comments about the dollar’s standing.

The trade-weighted Dollar Index has fallen 11 percent since President Barack Obama’s inauguration in January, in part because of a budget deficit projected to rise to $1.6 trillion this year as the government increases spending to boost the economy. The index measures the currency’s performance against the euro, yen, pound, Canadian dollar, Swiss franc and Swedish krona.

http://www.bloomberg.com/apps/news?pid=20601087&sid=aINN4BM6Fy5w#

By Daniel Whitten

Sept. 27 (Bloomberg) -- World Bank President Robert Zoellick said the U.S. shouldn’t take for granted the dollar’s status as the world’s main reserve currency.

In remarks set for delivery tomorrow, Zoellick said the “next upheaval” in the international economic order is under way as emerging nations gain greater influence.

“The United States would be mistaken to take for granted the dollar’s place as the world’s predominant reserve currency,” according to excerpts released by the World Bank.

Policy makers from China to Russia repeatedly have called for an alternative to the world’s main currency in foreign- exchange reserves.

Zoellick’s speech to the Paul H. Nitze School of Advanced International Studies at Johns Hopkins University in Washington echoes his previous comments about the dollar’s standing.

The trade-weighted Dollar Index has fallen 11 percent since President Barack Obama’s inauguration in January, in part because of a budget deficit projected to rise to $1.6 trillion this year as the government increases spending to boost the economy. The index measures the currency’s performance against the euro, yen, pound, Canadian dollar, Swiss franc and Swedish krona.

http://www.bloomberg.com/apps/news?pid=20601087&sid=aINN4BM6Fy5w#

Buster

TSP Talk Royalty

- Reaction score

- 109

I certainly hope you have a great success story to tell your great grand children..I pray your prognosis is bright.Thanks guys.

")

Show-me

TSP Legend

- Reaction score

- 104

Welcome to the New Normal

http://seekingalpha.com/article/163553-welcome-to-the-new-normal

Welcome to the New Normal

September 27, 2009 John Mauldin

A Double-Dip Recession?

http://seekingalpha.com/article/163553-welcome-to-the-new-normal

Welcome to the New Normal

September 27, 2009 John Mauldin

Unemployment is high and rising. But if the recession is over, won't employment start to rise? The quick answer is no. We look deeper into the Statistical Recovery and find yet more reasons to be concerned about near-term deflation.

This week we consider all things unemployment and ponder the need to create at least 15 million jobs in the next five years to return to a full-employment economy - and the implications for both the US and world economies if we don't. Economic is often about what we can clearly see, and yet it is understanding what we can't see that gives us true insight. We start with a collection of facts that we can see and then begin a thought exercise to find the implications.

This headline unemployment number (9.7%) is what we see when we read the paper. What we typically don't see is the real number of unemployed. For instance, if you have not actively looked for a job in the last four weeks, even if you would like one, you are not counted as unemployed. You are called a "marginally attached" or "discouraged" worker. Often there are very good reasons for this. You could be sick, dealing with a family emergency, going back to school, or not have transportation.

Right now, about one-third of marginally attached workers actively want jobs but have not bothered to look because they believe there are no jobs in their area, at least not for them. If you add that extra 758,000 to the unemployment data, you get what is called U-4 unemployment, which today is 10.2%. If you count all marginally attached workers the unemployment number is 11% (U-5 unemployment).

And if you add those who are employed part-time for economic reasons (i.e., they can't get full-time jobs) the unemployment number rises to 16.8%. (That is called U-6 unemployment.)

David wrote in a special report Friday:

What does all this mean? It means that when the economy does begin to recover, when we finally get to the other side of the mountain, companies are going to raise their labour input first by lifting the workweek from its record low. Just to get back to the pre-recession level of 33.8 hours would be equivalent to hiring three million workers. And, the record number of people working part-time against their will are going to be pushed back into full-time, which will be great news for them, but not so great news for the 125,000 - 150,000 new entrants into the labour market every month.

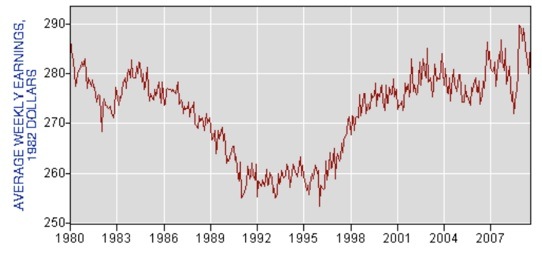

Then there is the matter of average weekly earnings. If you adjust for inflation, workers are making roughly what they did in 1980. The chart is straight from the BLS website.

And What We Don't See

Those are the facts. Now it's time to look at what we don't see, and what you don't read or hear from the mainstream media.

We saw above that we are adding about 1.5 million workers to the workplace every year. That means over the next five years we are going to need 7.5 million jobs just to maintain that growth, or about 125,000 a month. That is on the low side of what economists normally estimate, which is around 150,000 per month. If we used the 150,000 estimate, it would mean we need 9 million jobs.

There are at least 1 million (and probably more like 2 million) discouraged workers who would take jobs if the economy got better. You can derive that number by going back to early 2007 and seeing the level of discouraged workers. That means, by the end of 2014 we are going to have 163 million people in the work force (see table above).

Today we have 139.6 million jobs, and that number is likely to slip at least another half million (last month the economy lost 216,000 jobs, with a very suspicious birth-death ratio accounting for a lot of job creation). So let's call it 139 million current jobs.

Let's assume that we would like to get back to a 5% unemployment rate. That would not be stellar, but it would certainly be better than where we are today. Five percent unemployment in late 2014 will mean 8.1 million unemployed. To get to 5% unemployment we will have to create 14 million jobs in the five years from 2010-2014. (163 million in labor pool minus 8 million unemployed is 155 million jobs. We now have 139 million jobs, so the difference is roughly 15 million.) Plus the equivalent of 3 million jobs that Rosenberg estimates, just to get back to an average work week. And maybe the extra 1.5 million a year I mentioned above.

But let's ignore those latter jobs and round it off to 15 million. Let's hope that by the beginning of next year we stop losing jobs. That means that to get back to 5% unemployment within five years we need to see, on average, the creation of 250,000 jobs per month. As an AVERAGE!!!!!

Look at the table below. It is the number of jobs added or lost for the last ten years. Do you see a year that averaged 250,000? No.

If you take the best year, which was 2006, you get an average monthly growth of 232,000. If you average the ten years from 1999, you get average monthly job growth of 50,000. If you take the average job growth from 1989 until now, you get an average of 91,000 a month. If you take the best ten years I could find, which would be 1991-2000, the average is still only 150,000. That is a long way from 250,000.

A Double-Dip Recession?

And that is before this administration makes the economically suicidal move to raise the top tax rate by 10%. The popular image is that those who pay the highest tax rate are Wall Street execs, bankers, and corporate moguls. The reality is that 75% of them are small business owners, and they are responsible for the large majority of new jobs that are going to be needed, not to mention a large part of consumer spending. If you tax them more you are going to get fewer jobs (as they will have less to invest) and less consumer spending.

A tax increase of the size being contemplated, with unemployment at today's level, will guarantee a double-dip recession, which of course means that unemployment will rise, not fall. Go back and look at that chart on unemployment. Notice the very steep rise in the second recession of the early '80s. That is what we could be facing.

I stopped by to visit my #2 daughter (Melissa) last night. She works in a local watering hole while going to school. It is quite popular and is usually quite crowded. Last evening it was untypically quiet.

I asked, "What's up?" The manager and Melissa began talking about how slow things were getting, about how friends who were regulars had lost their jobs and had to move back in with parents. With few exceptions, it is slower than a few years ago everywhere I go. A recent Gallop poll said 71% of people are cutting back and 90% are watching what they are spending. 33% said their companies are cutting back on hiring.

Every poll or survey I see shows businesses deciding to cut back. Talking with my kids (the six who are young and in the work force), it is a rather difficult time. But then I think that I had to enter the workforce in 1975, not a very good year or decade. And we all made it, if not very easily. We lived very modestly (to say the least) for those first years.

And so it goes. Each generation has to learn how to deal with adversity and the problems of starting out. Many of those in my generation are now trying to figure out how to deal with a retirement that does not look nearly as comfortable as it did a few years ago.

I still hope we can muddle through.

Your 'glad to get to 60' analyst.

WorkFE

TSP Legend

- Reaction score

- 535

Thanks Show-Me excellant read.

My wife and I are heavy travelers in the summer. This summer we put 4000 miles on our travel trailer. Although the places we visited were packed, I did notice a different kind of spending while traveling. People are being thrifty.

My wife and I are heavy travelers in the summer. This summer we put 4000 miles on our travel trailer. Although the places we visited were packed, I did notice a different kind of spending while traveling. People are being thrifty.

Show-me

TSP Legend

- Reaction score

- 104

Bank of America, 3 Other Banks’ FDIC Fees May Top $10 Billion

By David Mildenberg

Sept. 29 (Bloomberg) -- The Federal Deposit Insurance Corp.’s plan to bolster its reserves may cost Bank of America Corp. and three of the largest U.S. banks more than $10 billion.

Bank of America, the biggest U.S. lender by deposits, may owe $3.5 billion under the FDIC proposal for banks to prepay three years of premiums, based on the lowest assessment rate multiplied by the bank’s $900 billion in second-quarter U.S. deposits.

“This seems like a very hefty amount,” said Tim Yeager, a finance professor at the University of Arkansas and former economist at the Federal Reserve Bank of St. Louis. “The FDIC’s projections of future losses are pretty severe, and they are trying everything they can to avoid tapping the Treasury.”

U.S. bank premiums range from 12 cents per $100 in deposits for the safest lenders to 45 cents for banks the U.S. considers risky, said Chris Cole, senior regulatory counsel for the Independent Community Bankers of America. The FDIC proposed asking banks to pay premiums for the fourth quarter and next three years on Dec. 30. The fees will raise $45 billion.

The FDIC is required by law to rebuild the fund when the reserve ratio, or the balance divided by insured deposits, falls below 1.15 percent. It was 0.22 percent on June 30 and will sink to a deficit tomorrow. The fund, drained by 95 bank failures this year, had $10.4 billion at the end of the second quarter. The fund will erase its deficit by 2012, the FDIC said today.

more.......

http://www.bloomberg.com/apps/news?pid=20601087&sid=aaZTaeysFJPY#

Will it be enough?

Warrenlm

TSP Legend

- Reaction score

- 93

Denninger made a bid deal of the FDIC call for premium prepayment but "the new normal" thinking should include the government-banking relationship, too. Treasury and Fed have so intertwined billions/trillions in the banks, who is to say that a few billion from one pocket to another is anything to write about? Theory is out the window and the only thing that matters is whether other nations will both renew their Treasury holdings and also buy additional offerings. We've become like Travlolta in a Civil Action continually asking the banker for a little more. The fact that standards previously thought significant (insolvency) are violated is not going to change the "cooperation" between Treasury, Fed and the big banks.

Show-me

TSP Legend

- Reaction score

- 104

Theory is out the window and the only thing that matters is whether other nations will both renew their Treasury holdings and also buy additional offerings.

Yes, the trillion dollar question! Will other nations buy our T-bills? The Fed has been doing what they do best by keeping the T-bills rates artificially low by buy up tons of them. What happens when they slow and then stop?

I see this. The end near.....................for the cheap money. The 10 year T-bill is ties to mortgage rates, it will go up if the Fed allows a free market. Mortgages go up, people get concerned. Reported yesterday, home prices are jumping up. Inflation. Jobs.

Inflation I see a different way after reading a story on money supply. Basically as loans are defaulted on and written of by lenders that money supply is taken off the books. Poof, gone. So all those loan defaults are actually helping reduce money supply and inflation. Sucks for the lender but curbs inflations a bit. Inflation is coming but it will take a little longer.

Biggest point is jobs. The Fed can jack around with rates and T-bills all it wants but jobs will grow the economy.

Please read "Welcome to the new normal", to get to back to JUST 5% unemployment we need to created 250,000 jobs a month for five years.

Do you really see that happening?

After seeing the Peter Schiff video in Poolmans thread, I am rethinking the idea of moving out of the Country after I retire. I will keep buying gold and silver bullion. Some place not crowded.

Show-me

TSP Legend

- Reaction score

- 104

The Labor Department's latest reading on weekly unemployment shows new jobless claims rose more than expected to 551,000, evidence that jobs remain scarce. Economists had predicted claims to rise to 535,000.

The Commerce Department says consumer spending surged by the largest amount in nearly eight years in August, as personal incomes lag. Consumer spending rose 1.3 percent in August and incomes edged up 0.2 percent.

http://finance.yahoo.com/news/Stock...html?x=0&sec=topStories&pos=main&asset=&ccode=

Ouch! Sounds like the herd is getting weak on the saving or are getting painted in a corner.

Show-me

TSP Legend

- Reaction score

- 104

No kidding Ben! LOL

Bernanke Sees Risk To Dlr On Horizon If US Debt Not Contained

By Tom Barkley

Of DOW JONES NEWSWIRE

WASHINGTON (Dow Jones)--U.S. Federal Reserve Chairman Ben Bernanke waded into the international debate over the fate of the dollar Thursday, pledging to do his part to avoid what he sees as a longer-term risk to the dollar's status as the world's predominant reserve currency.

China and Russia have been the major drivers behind calls for an alternative reserve currency, blaming the U.S. for the global crisis and worried that its growing debt load could pose a further threat to stability. That view gained some additional force this week when World Bank President Robert Zoellick predicted that the dollar would face increasing as a reserve currency and its status would depend on how well the U.S. can manage its debt.

Representatives Michele Bachmann of Minnesota and Bill Posey of Florida, two Republicans that have been critical of the Obama administration's stimulus package and other spending measures, sought agreement from the Fed chairman during a House Financial Services Committee hearing.

Asked by Bachmann to respond to Zoellick's remarks, Bernanke cited two areas of agreement.

The Fed chief said he agreed with Zoellick that "there's no immediate risk to the dollar, it's a relatively long-term issue."

"I also agree with him, though, that if we don't get our macro[economic] house in order that that will put the dollar in danger, and that the most critical element there is long-term fiscal stability," he said.

more...........

http://online.wsj.com/article/BT-CO-20091001-713464.html

Bernanke Sees Risk To Dlr On Horizon If US Debt Not Contained

By Tom Barkley

Of DOW JONES NEWSWIRE

WASHINGTON (Dow Jones)--U.S. Federal Reserve Chairman Ben Bernanke waded into the international debate over the fate of the dollar Thursday, pledging to do his part to avoid what he sees as a longer-term risk to the dollar's status as the world's predominant reserve currency.

China and Russia have been the major drivers behind calls for an alternative reserve currency, blaming the U.S. for the global crisis and worried that its growing debt load could pose a further threat to stability. That view gained some additional force this week when World Bank President Robert Zoellick predicted that the dollar would face increasing as a reserve currency and its status would depend on how well the U.S. can manage its debt.

Representatives Michele Bachmann of Minnesota and Bill Posey of Florida, two Republicans that have been critical of the Obama administration's stimulus package and other spending measures, sought agreement from the Fed chairman during a House Financial Services Committee hearing.

Asked by Bachmann to respond to Zoellick's remarks, Bernanke cited two areas of agreement.

The Fed chief said he agreed with Zoellick that "there's no immediate risk to the dollar, it's a relatively long-term issue."

"I also agree with him, though, that if we don't get our macro[economic] house in order that that will put the dollar in danger, and that the most critical element there is long-term fiscal stability," he said.

more...........

http://online.wsj.com/article/BT-CO-20091001-713464.html

Show-me

TSP Legend

- Reaction score

- 104

The Good, the Bad, and the Ugly.

The Good: Pending home sales increased by 6.4%, construction spending .8%, and personal spending up 1.3%.

The Bad: Initial Claims was 551k, personal income .2%, and ISM 52.6.

The Ugly: Pending home sales could be fueled by stimulus tax credit. Saturn in the can, Ken Lewis retires with bonus, still need 250k jobs a month average to get back to 5% unemployment in FIVE years, Ben seen the light on weak dollar, printing money still a option, IMF expects $1.2 trillion in bank write downs next year.

It's all good.

The Good: Pending home sales increased by 6.4%, construction spending .8%, and personal spending up 1.3%.

The Bad: Initial Claims was 551k, personal income .2%, and ISM 52.6.

The Ugly: Pending home sales could be fueled by stimulus tax credit. Saturn in the can, Ken Lewis retires with bonus, still need 250k jobs a month average to get back to 5% unemployment in FIVE years, Ben seen the light on weak dollar, printing money still a option, IMF expects $1.2 trillion in bank write downs next year.

It's all good.Show-me

TSP Legend

- Reaction score

- 104

WE ARE NOT HUMAN BEINGS GOING THROUGH A TEMPORARY SPIRITUAL EXPERIENCE.

WE ARE SPIRITUAL BEINGS GOING THROUGH A TEMPORARY HUMAN EXPERIENCE.

Got this in a email this morning, thought it was catchy.

Show-me

TSP Legend

- Reaction score

- 104

http://finance.yahoo.com/focus-reti...-a-big-nest-egg.html?mod=fidelity-startingout

If you eliminate $100 of wasteful spending per month and instead channel that cash to an investment vehicle that yields an annual interest rate of 10%, that translates to more than $75,000 over 20 years, and more than $500,000 over the course of 40 years. Granted, the buying power of figure is chewed up by inflation, but the prudent person still reaps the benefits of not wasting cash on unnecessary things.

Starting principal balance: $0

Monthly investment payments: $100

Interest rate: 10%

Future value: 20 years = $75,936

Future value: 40 years = $632,408

Starting principal balance: $0

Monthly investment payments: $250

Interest rate: 10%

Future value: 20 years = $189,842

Future value: 40 years = $1,581,019

If someone were motivated enough to find $500 a month and put it away in the form of investment payments, the results lead to an exponential increase in comfort during one's retirement. With an annual rate of return of 10% over 40 years, the figure approaches $3 million for your nest egg.

Starting principal balance: $0

Monthly investment payments: $500

Interest rate: 10%

Future value: 20 years = $379,684

Future value: 40 years = $3,162,039

How much more would your nest egg be if you work for a company that matches your 401(k) dollar for dollar up to a certain amount? Given that the federal government's social safety net programs such as Social Security and Medicare are expected to hit fiscal challenges as the baby boomers retire, such anticipated uncertainties encourage individuals to take their retirement circumstances into their own hands. Secondly, the high cost of healthcare in the United States is a primary driver for individuals and couples filing for personal bankruptcy. The power of compound interest can help one to avoid financial straits in the future.

hessian

TSP Analyst

- Reaction score

- 23

Hi Show-me,WE ARE NOT HUMAN BEINGS GOING THROUGH A TEMPORARY SPIRITUAL EXPERIENCE.

WE ARE SPIRITUAL BEINGS GOING THROUGH A TEMPORARY HUMAN EXPERIENCE.

Its been awhile, this market's just been too confusing for me (what analysts to believe?), anyway - wanted to pass along...

a. Tremendous quote!!

b. I'm going to pass along your the savings/interest scenarios to my niece and nephew.

c. Maybe an interesting article (for today/this week)...

http://money.cnn.com/2009/10/03/markets/sunday_lookahead/index.htm

mayday

TSP Pro

- Reaction score

- 17

show

that was a good scenario you shared with us. i have been telling my 2 young boys that saving early is the KEY !!! wish someone would have told me that when I was buying beer and having fun when I got out of high school !!!

thanks

john

Hey John; It's a good thing having fun in high school.

CapeChem

TSP Strategist

- Reaction score

- 4

show

that was a good scenario you shared with us. i have been telling my 2 young boys that saving early is the KEY !!! wish someone would have told me that when I was buying beer and having fun when I got out of high school !!!

thanks

john

Most likely you were told over and over again......but you just didnt listen...that would be typical of a high school student.

- Status

- Not open for further replies.